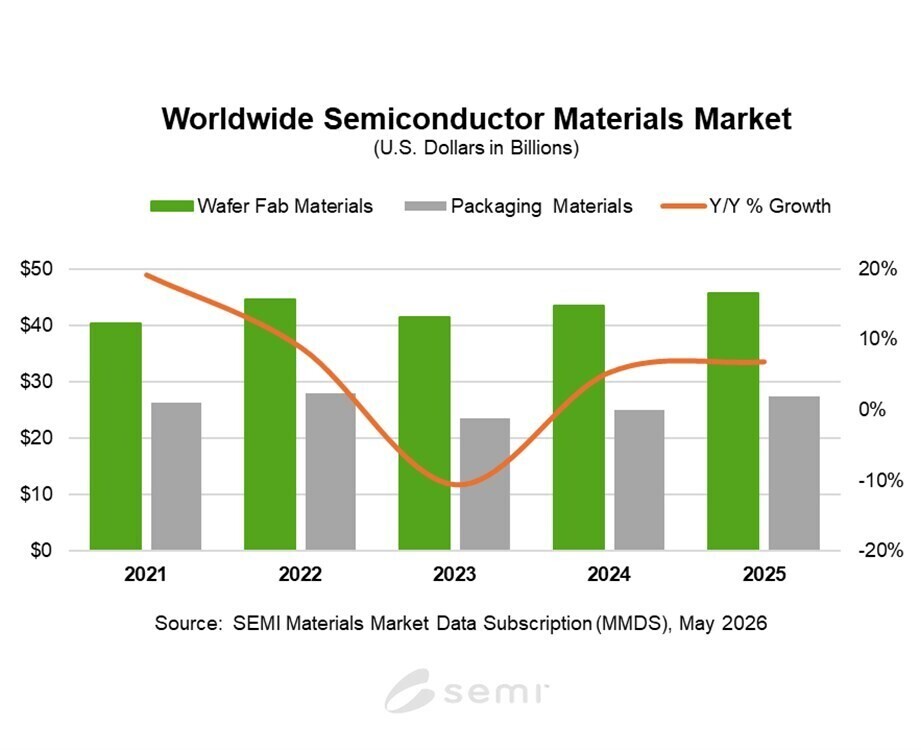

The semiconductor materials market closed 2025 at its highest point ever, reaching $73.2 billion—a figure that reflects the relentless march of chipmaking complexity. This milestone underscores how even a single year can reshape the landscape for PC builders and system designers, pushing efficiency to new extremes.

Two segments led the charge: wafer fabrication materials climbed 5.4% to $45.8 billion, while packaging materials jumped 9.3% to $27.4 billion. The shift is visible in everything from lithography chemicals to bonding wire, where gold prices and substrate demand are now setting the pace for regional growth.

Regional shifts redefine the market

- Wafer fab materials: $45.8 billion (up 5.4%) – Lithography-related chemicals saw double-digit gains, a direct result of tighter process requirements at advanced nodes.

- Packaging materials: $27.4 billion (up 9.3%) – Substrates and bonding wire drove growth, with gold prices and advanced substrate demand pulling the segment forward.

Taiwan maintained its dominance as the largest consumer at $21.7 billion, but China’s double-digit expansion—now at $15.6 billion—has narrowed the gap. South Korea followed with $11.2 billion, while Europe remained the only region without year-over-year growth.

What this means for PC builders

For those assembling high-performance systems, the implications are clear: material costs are rising faster than ever, but so is the performance per watt. Advanced-node demand isn’t just about raw speed; it’s about efficiency gains that trickle down to real-world power consumption. A user might notice longer battery life in a laptop or cooler operation in a desktop build—small improvements that add up when multiplied across millions of systems.

China and North America are the engines behind this growth, with both regions seeing double-digit increases. The data suggests that investments in high-bandwidth memory and high-performance computing are outpacing other sectors, a trend that will likely shape upgrade decisions for years to come.

The market’s trajectory is now set on a two-year forecast, but the confirmed numbers paint a picture of sustained pressure on material suppliers—and opportunity for those who can navigate it. The biggest beneficiaries will be PC builders who prioritize efficiency without sacrificing performance, a balance that has never been more critical.