The semiconductor foundry industry is entering a period of sharp contrast. On one hand, AI workloads—particularly for GPUs and TPUs—are sustaining advanced-node production at record levels. On the other, mature-node segments face growing uncertainty as memory prices rise, casting doubt on demand for mainstream end devices later this year.

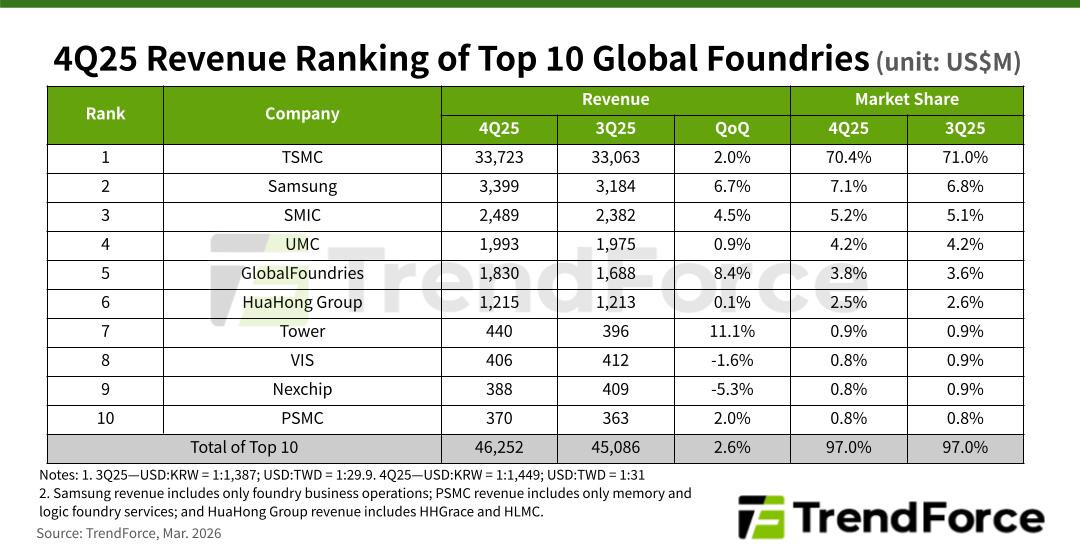

In 4Q25, the combined revenue of the world’s top ten foundries climbed 2.6% quarter-over-quarter to nearly $46.3 billion, according to latest research. This follows a 26.3% year-over-year jump in 2025, setting a new industry benchmark. Yet beneath these numbers lies a more complex story: while AI server components remain in tight supply, the path forward is far from clear.

Key Specs at a Glance

- Revenue: $46.3 billion (top 10 foundries, 4Q25)

- YoY Growth: 26.3% (2025 total)

- Node Focus: 3 nm and 2 nm production driving ASPs

- Supply Dynamics: AI GPUs and TPUs sustaining advanced-node utilization

The data reveals a two-tiered market. TSMC, still the dominant player with 70.4% share, saw a slight dip in wafer shipments but offset this with strong demand for its 3 nm node—particularly from flagship smartphone APs like those powering the iPhone 17 series. Samsung Foundry, meanwhile, returned to profitability after a period of volatility, growing revenue 6.7% QoQ to $3.4 billion while expanding its market share to 7.1%. The shift reflects gains in 2 nm production and logic dies for HBM4 memory, though overall fab utilization remains a concern.

What’s Next: Pricing and Uncertainty

The outlook for 2026 is mixed. Early inventory builds could stabilize utilization in the first half of the year, but rising memory prices may dampen demand for non-AI products by mid-year. This could pressure ASPs in mature nodes, particularly for PMICs and server peripherals. Meanwhile, emerging applications like silicon photonics (SiPho) and silicon-germanium (SiGe) are showing steady growth, suggesting niche opportunities—but whether they’ll scale enough to offset broader market softening remains an open question.

For AI workloads specifically, the focus is on sustaining supply for GPUs like the RTX 5090 and TPU chips. The 384-bit memory bus in next-gen GPUs (RDNA-based designs) demands precision manufacturing at 2 nm or finer, a challenge that only TSMC and Samsung are currently addressing. Yet even here, yield rates and pricing stability could become flashpoints if demand outpaces production capacity.

The bottom line: the foundry sector is navigating a tightrope between AI-driven growth and broader market uncertainty. What’s confirmed? Strong revenue in advanced nodes and gains for players like Samsung. What’s not yet clear? Whether mature-node segments can hold steady, or if pricing pressures will force another round of consolidation.