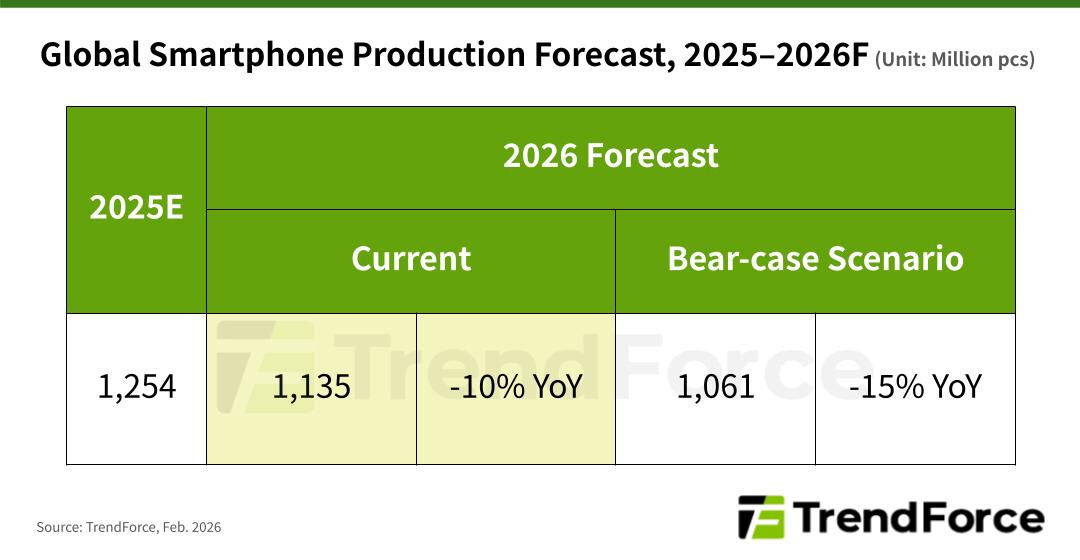

The smartphone market is bracing for its sharpest contraction in years, with global production expected to shrink by nearly 10% in 2026—down to roughly 1.135 billion units—due to a dramatic spike in memory costs. For brands relying on mid-range and entry-level models, the financial strain is already pushing production cuts deeper, with some analysts warning of a potential 15% drop in output if prices remain elevated.

Memory—once a modest 10-15% of a phone’s bill of materials—now accounts for 30-40% of costs, forcing manufacturers to either absorb losses, raise prices, or scale back production. The ripple effect is uneven: while premium brands like Apple and Samsung can better absorb the hit, budget-focused companies risk significant volume declines.

Key specs under pressure

- Memory configuration: An 8 GB RAM + 256 GB storage setup has seen contract prices surge nearly 200% year-over-year in early 2026.

- Cost impact: Memory now represents 30-40% of a smartphone’s total bill of materials, up from 10-15% historically.

- Production forecasts: Global output could fall 10-15% YoY, with regional and brand-specific variations.

The crisis isn’t just about cost—it’s about survival. Brands with vertically integrated supply chains, like Samsung, are better positioned to mitigate losses. Apple, too, benefits from a premium customer base willing to pay more. But for companies like Xiaomi and Transsion, which target price-sensitive markets, the margin for error is slim. Even raising prices risks losing demand in regions where affordability is key.

Who’s holding steady—and who’s cutting back?

Samsung, the world’s largest smartphone manufacturer and a major memory supplier, is expected to see a smaller production decline than Chinese competitors. Its vertical integration—controlling both memory production and device assembly—provides a buffer. Apple, meanwhile, faces less immediate pressure thanks to its high-end positioning and loyal customer base. Premium models can absorb higher memory costs without alienating buyers.

In contrast, brands like Xiaomi and Transsion—heavily reliant on mid-range and entry-level devices—are in a far tougher spot. Their price-sensitive markets offer little room to pass costs to consumers. If memory prices don’t ease, these companies may need to reduce production by double digits, further squeezing their market share.

Huawei’s unexpected advantage

One outlier in this downturn is Huawei. Despite operating in a competitive Chinese market, the company’s strong brand loyalty and flexible pricing strategies give it an edge. With its HarmonyOS ecosystem expanding and a customer base less sensitive to price hikes, Huawei could even see production growth in 2026—while others shrink.

The broader industry faces a double whammy: rising costs and weakening demand. Smartphones today already exceed most users’ needs, slowing replacement cycles. Even if memory prices stabilize, the structural shift in consumer behavior may persist, leaving brands scrambling to adapt.

For now, the message is clear: the smartphone industry is at a crossroads. Those who can’t adjust—whether through pricing, product mix, or supply chain control—risk being left behind.