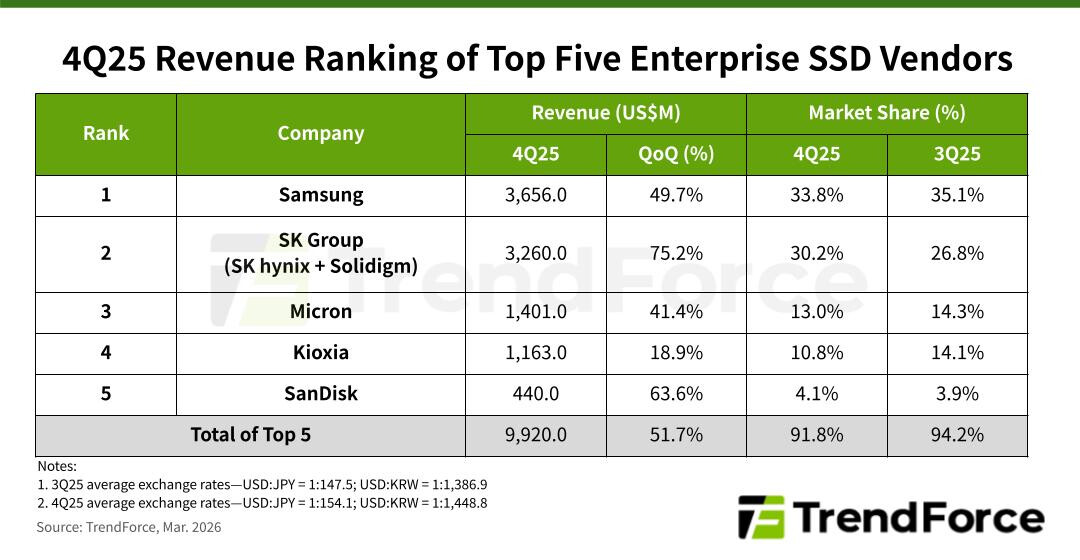

The enterprise SSD market is undergoing a rapid transformation, with revenue for the top five vendors jumping over 51.7% quarter-over-quarter to exceed $9.9 billion in Q4 2025. This surge reflects a fundamental shift in data center needs, where AI inference workloads and server refresh cycles have created unprecedented demand for high-performance storage solutions.

Among the leading vendors, SK Group emerged as the standout performer, with its revenue growing over 75% to reach $3.26 billion. This growth was fueled by strong demand for high-capacity QLC SSDs, which are increasingly being adopted in AI-driven environments. The group's market share climbed to 30.2%, reflecting its strategic focus on differentiating technology and addressing the evolving needs of generative AI workloads.

Samsung maintained its position as the top vendor with nearly $3.66 billion in revenue, up 49.7% quarter-over-quarter. The company's vertically integrated business model, which includes its own DRAM and NAND Flash production, has provided a stable supply chain for its SSD offerings. Samsung has also fully rolled out its 176-layer QLC enterprise SSD lineup, setting the stage for significant shipment growth in 2026.

Micron ranked third with revenue exceeding $1.4 billion, representing a 41.4% increase. The company has strategically reduced its focus on consumer SSDs, concentrating instead on high-margin enterprise solutions. Micron is also developing SLC SSDs with high drive-writes-per-day (DWPD) ratings to support AI workloads, particularly key-value (KV) cache operations, which are expected to become a crucial part of its AI storage strategy.

Kioxia generated $1.16 billion in revenue, up 18.9% quarter-over-quarter. While its growth lagged behind some competitors, the company is investing heavily in long-term opportunities related to AI storage. Its current strategy focuses on expanding its portfolio of high-speed and high-endurance SSD products to meet future demand from KV cache workloads and AI training.

Sandisk reported revenue of $440 million, rising 63.6% quarter-over-quarter. Although its revenue base remains smaller than its peers, the strong growth rate is noteworthy. The company is expected to significantly increase the share of QLC-based SSD shipments in 2026, which should drive a meaningful rise in the contribution from enterprise products.

Looking ahead, PCIe 5.0 is poised to become the mainstream interface for enterprise SSDs in 2026. However, competition among suppliers will not be solely determined by NAND layer counts. Instead, leadership will increasingly depend on which companies can deliver stable PCIe 6.0 solutions first and develop SSD products optimized specifically for AI workloads.

- Key Specifications:

- PCIe 5.0: Expected to become the mainstream interface in 2026

- Revenue Growth: Over 51.7% quarter-over-quarter for top five vendors

- Market Share: SK Group's market share climbed to 30.2%

The surge in enterprise SSD demand is a clear indicator of the broader shift towards AI-driven data center workloads. For businesses considering upgrades, this trend underscores the importance of investing in high-performance storage solutions that can handle the demands of modern AI applications. The focus on PCIe 5.0 and the development of PCIe 6.0 solutions will be critical for companies looking to future-proof their infrastructure.

In summary, the enterprise SSD market is at a pivotal moment, with significant growth potential driven by AI workloads and server upgrades. Companies that can deliver stable and optimized solutions will be best positioned to capture this opportunity and shape the future of data storage.