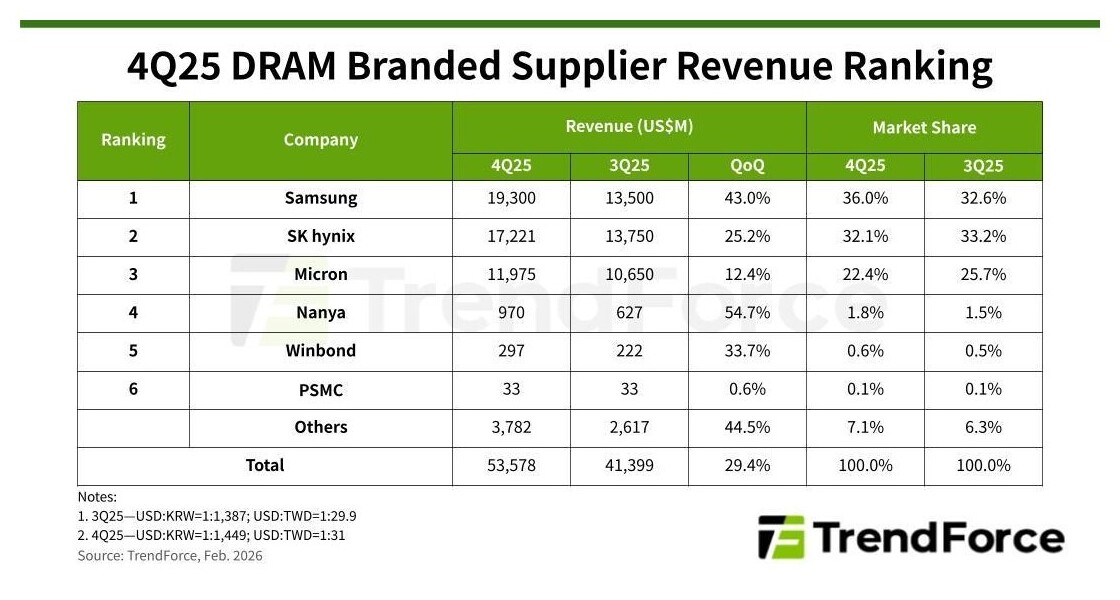

Thursday, February 26th 2026 DRAM Market Grows 29% in 4Q25, Samsung Regains Top Spot Press Release by Nomad76 Today, 07:56 Discuss (3 ) TrendForce's latest findings reveal that the expansion of AI applications from LLM training to inference has prompted CSPs to broaden data center build-outs beyond AI servers to include general-purpose servers. This shift has extended memory procurement beyond HBM3e, LPDDR5X, and high-capacity RDIMMs to RDIMMs across multiple densities. Aggressive additional orders have driven a sharp increase in conventional DRAM contract prices, lifting total DRAM industry revenue to $53.58 billion in 4Q25, up 29.4% QoQ. Across segments, buyers have struggled to secure sufficient supply amid a widening supply-demand gap. This has significantly strengthened suppliers' pricing power. Conventional DRAM contract prices rose 45-50% QoQ, while blended contract prices for conventional DRAM and HBM increased 50-55%, marking an accelerated upswing across all product categories. Looking ahead to 1Q26, seasonal weakness in consumer demand is expected to constrain bit shipment growth, potentially flattening sequential growth for suppliers. However, as CSPs prioritize securing supply and remain receptive to higher procurement prices, other application segments must follow suit to maintain allocation. TrendForce projects further acceleration in contraction price increases in 1Q26, with conventional DRAM prices expected to surge 90-95% QoQ, and blended conventional DRAM + HBM pricing rising 80-85% QoQ. Samsung's 4Q25 revenue climbed to $19.30 billion, up 43% QoQ, lifting its market share by 3.4 percentage points to 36%, allowing it to reclaim the top position. ASPs rose approximately 40% QoQ—the strongest among the top three vendors—while bit shipments grew in the low-single-digit range, supported by HBM business expansion and in line with company guidance. SK hynix posted revenue of $17.22 billion, up 25.2% QoQ, though its market share slipped 1.1 percentage points to 32.1%, ranking second. ASPs increased in the mid-20% range QoQ, reflecting a higher HBM revenue contribution—where contract price volatility is comparatively lower—than its peers. Bit shipments rose in the low-single-digit range, consistent with guidance. Micron reported revenue of $11.98 billion, up 12.4% QoQ, with market share declining 3.3 percentage points to 22.4%, maintaining third place. ASPs increased approximately 17% QoQ—the lowest among the top three vendors—while bit shipments declined about 4% sequentially. This reflects earlier contract price negotiations compared with Korean peers, resulting in comparatively lower realized pricing levels. Taiwan-based DRAM suppliers continued strong momentum from 2Q25, with most reporting sequential revenue growth exceeding 30% in 4Q26. These vendors primarily focus on mature-node products, filling supply gaps created as leading suppliers transition production to advanced nodes. Nanya's revenue surged 54.7% QoQ to $970 million. Bit shipments increased in the low-teens percentage range, while ASPs rose in the 30% range. Operating margin expanded sharply from 6% to 39.1%, driven by substantial contract price increases for DDR4 and DDR3, continued restocking from major customers, and strategic capacity relocation of 20 nm and 1B products nodes toward higher-margin DDR4 products. Winbond reported revenue of $297 million, up 33.7% QoQ, with bit shipments growing in the low-single-digit range and ASPs rising in the mid-30% range. Growth was driven by increased shipments of 20 nm DDR4 4 Gb products. PSMCs' reported DRAM revenue, excluding foundry services, rose 0.6% QoQ to $33 million. Including foundry-related DRAM revenue, total DRAM-related revenue increased approximately 5% QoQ. Following its licensing agreement with Micron for process technology, PSMC is expected to accelerate the next phase of DRAM capacity expansion. Source: TrendForce Related News Tags: DDR DDR3 DDR4 DDR5 DIMM DRAM Financial Results HBM LPDDR5 LPDDR5X market Micron Nanya production PSMC RAM RDIMM Samsung SK hynix Taiwan Winbond Jul 23rd 2025 DDR6 Memory Arrives in 2027 with 8,800-17,600 MT/s Speeds (174) Jan 16th 2026 NVIDIA Reportedly Ends GeForce RTX 5070 Ti Production, RTX 5060 Ti 16 GB Next (210) Dec 31st 2025 Leaks Predict $5000 RTX 5090 GPUs in 2026 Thanks to AI Industry Demand (124) Dec 13th 2025 SK Hynix Forecasts Tight Memory Supply Lasting Through 2028 (118) Dec 3rd 2025 Micron to Exit Crucial Consumer Business, Ending Retail SSD and DRAM Sales (195) Feb 6th 2026 NVIDIA to Use SK hynix and Samsung HBM4 for Vera Rubin Without Micron (7) Nov 24th 2025 Chinese CXMT Shows Homegrown DDR5-8000 and LPDDR5X-10667 Memory (12) Nov 18th 2025 AMD & NVIDIA Reportedly Consider GPU Cuts, ASUS and Others Slow Motherboard Plans Amid Memory Shortage (36) Nov 27th 2025 NVIDIA May Stop Bundling Memory with GPU Kits Amid GDDR Shortage (20) Feb 6th 2026 Major PC OEMs Reportedly Exploring Chinese CXMT Memory Amid Shortages (32) Add your own 3 on DRAM Market Grows 29% in 4Q25, Samsung Regains Top Spot #1 Philaphlous Well no ____ sherlock. This report is so misleading because the growth has nothing to do with actual product volume and all to do with pricing. Not saying anything bad about the TPU writing of the article, but more trendforce's analysis. That's why car manufacture's release numbers by units produced/delivered rather than $dollars produced/delivered. With the 2-4x prices of DRAM it's no wonder prices of shipments are up and units actually produced could have been significantly less... The bigger tell-tale sign would be gross margin for some DRAM manufactures....I would expect that to go through the roof... #2 Nomad76 News PhilaphlousWell no ____ sherlock. This report is so misleading because the growth has nothing to do with actual product volume and all to do with pricing. Not saying anything bad about the TPU writing of the article, but more trendforce's analysis. That's why car manufacture's release numbers by units produced/delivered rather than $dollars produced/delivered. With the 2-4x prices of DRAM it's no wonder prices of shipments are up and units actually produced could have been significantly less... The bigger tell-tale sign would be gross margin for some DRAM manufactures....I would expect that to go through the roof...The number of units sold is a closely guarded secret (in most cases), as it can be exploited when you sell the same product to multiple customers in direct competition. #3 Wirko PhilaphlousWell no ____ sherlock. This report is so misleading because the growth has nothing to do with actual product volume and all to do with pricing. Not saying anything bad about the TPU writing of the article, but more trendforce's analysis. That's why car manufacture's release numbers by units produced/delivered rather than $dollars produced/delivered. With the 2-4x prices of DRAM it's no wonder prices of shipments are up and units actually produced could have been significantly less... The bigger tell-tale sign would be gross margin for some DRAM manufactures....I would expect that to go through the roof...Read the entire PR, there's enough info in it. Not absolute numbers but percentage changes in ASPs and bit shipments are all there.