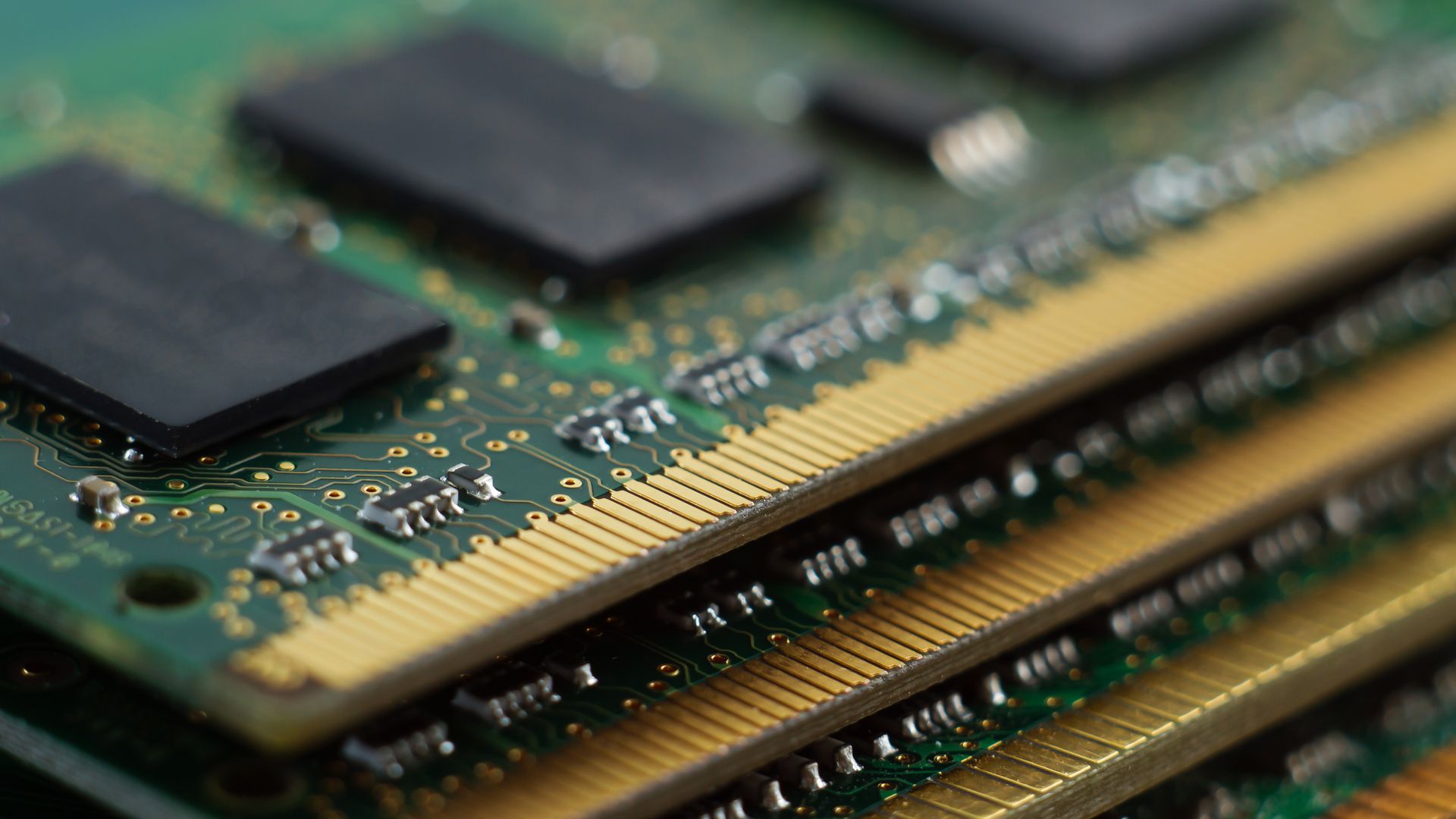

RAM prices have stopped climbing, but the respite is superficial. Behind the plateau, a complex web of supply chain constraints continues to squeeze manufacturers, especially those targeting budget segments.

The pause in price hikes comes after months of volatility triggered by geopolitical disruptions and shifting global demand. Yet the underlying issues—tight supply, high production costs, and limited availability of key components—persist. Industry observers note that while spot prices may appear stable, the broader ecosystem remains under pressure.

Specs in focus

- Current RAM pricing: no significant upward movement for standard DDR5 modules (16 GB–32 GB kits).

- Supply constraints: limited capacity expansion due to semiconductor fab bottlenecks.

- Impact on entry-level devices: reduced offerings from major brands, particularly in sub-1000 USD laptops.

The stabilization does not translate to abundant supply. Leading memory module manufacturers report that while they have avoided aggressive price hikes, internal production costs remain elevated. This has led to a shift away from low-margin products, including budget laptops and desktops, which now account for a smaller share of total shipments.

Deeper challenges

The RAM market’s fragile balance is further complicated by regional imbalances in chip production. Fab utilization rates in key regions have not recovered to pre-pandemic levels, meaning that even if demand softens, supply will not automatically catch up. This creates a scenario where prices could spike again on short notice.

For enterprise buyers, the implications are clear: while current contracts may lock in stable pricing, future procurement strategies must account for potential volatility. The lack of large-scale inventory buffers means that sudden demand surges—whether from AI workloads or seasonal cycles—could quickly tighten supply and push costs higher once more.

Workload impact

The stabilization does not solve the core problem: RAM is still a critical bottleneck for high-performance computing. Data centers, gaming rigs, and AI training setups all rely on consistent, affordable module availability. Without sustained improvements in fab capacity or breakthroughs in memory technology (such as HBM advancements), the market will remain vulnerable to disruption.

In practical terms, this means that enterprise IT teams must balance cost efficiency with risk mitigation. Stockpiling RAM is not a long-term solution, but neither is assuming stability. The most resilient approach may involve diversifying suppliers and hedging against regional production risks—strategies that were less critical before the current supply chain upheaval.

Outlook

The plateau in RAM prices is a temporary lull, not a resolution. The fundamental constraints of semiconductor manufacturing mean that even if today’s spot markets appear calm, deeper structural issues remain unresolved. For now, manufacturers are navigating a narrow path: maintaining margins without alienating cost-sensitive customers. But the underlying tension will persist until capacity expands or new memory technologies mature enough to fill the gap.